CPO Prices Expected to Trade Between RM4,400 (USD1,062) and RM4,650 (USD1,123) as Palm Oil Supply Outlook Tightens

Crude palm oil (CPO) prices remained supported above RM4,450 in June, despite a sharp correction in energy prices following a temporary ceasefire agreement between the US and Iran. Elevated energy prices have been the primary factor supporting palm oil prices since the onset of the West Asia conflict, driven by favourable biodiesel economics. As energy prices gradually ease and the geopolitical risk premium diminishes, palm oil prices are increasingly reverting to underlying market fundamentals, particularly the outlook for production, exports and stocks.

Heading into July, palm oil prices are expected to be shaped by the following key factors:

US Soybean Oil Export Slowdown

The unusually high premium commanded by US soybean oil since March 2026 has significantly reduced its export competitiveness. US soybean oil exports fell by 69% in first five months of 2026, leaving global importers increasingly dependent on South American supplies.Tight Palm Oil Export Supply

Concerns are mounting over the availability of exportable palm oil supplies from Indonesia in the coming months, driven by stagnant production growth, rising domestic demand and front-loaded exports resulting from the government export interventions.Softer Import Demand

Vegetable oil stocks in major importing countries such as China and India have risen sharply, which could temporarily slow import demand. This likely reflects weaker near-term consumption amid inflationary pressures and softer economic conditions.

A Brief Market Recap

The US Trade Representative (USTR) has proposed new tariffs of 10% and 12.5% on imports from 60 countries following an investigation into goods allegedly produced using forced labour. The proposal comes after the US Supreme Court struck down President Trump’s reciprocal tariff measures in February 2026. A public hearing and stakeholder consultation are scheduled for 7 July 2026.

The Indonesian government has announced plans to channel exports of the country’s natural resources, including palm oil, through a state-owned enterprise. The initiative aims to improve export price transparency and curb transfer pricing practices that shift profits from Indonesia’s natural resources exports to lower-tax jurisdictions, resulting in revenue losses for the government.

Energy prices eased to a four-month low after the US and Iran reached a temporary ceasefire agreement, reducing the geopolitical risk premium in global markets. Gasoil prices on the ICE exchange fell to USD900 per tonne, while Brent crude oil on the CME exchange declined to USD73 per barrel by end-June, around 40% below its March peak.

Malaysia's Palm Oil Supply and Demand for May 2026

Table 1: Monthly statistics of Malaysian palm oil for May 2026 (MPOB, 2026).

Palm Oil Supply and Demand Dynamics in July: Key Changes and Trends

Malaysia’s palm oil production declined by 113,000 tonnes, or 6.9% month-on-month, to 1.51 million tonnes in May. The decline was partly attributed to oil palm trees entering a temporary resting phase following stronger-than-usual production between October 2025 and March 2026. In addition, May recorded two public holiday days compared with none in April, resulting in fewer harvesting days.

Meanwhile, the decline in exports during May was largely anticipated, as slower purchasing activity in March and April amid heightened price volatility was expected to translate into lower shipments in May and June.

Despite the monthly decline, cumulative exports from January to May 2026 increased by 783,000 tonnes or 13.8% year-on-year. The largest increases were recorded in exports to India, Kenya and Vietnam, which collectively rose by 749,000 tonnes.

Sub-Saharan Africa and ASEAN continue to emerge as important growth markets for Malaysian palm oil. During the first five months of 2026, these two regions accounted for 36% of Malaysia’s total palm oil exports, compared with 25% five years ago in 2022.

In the third quarter of 2026, Malaysia’s palm oil production is likely to record a year-on-year decline, while exports and domestic consumption are expected to remain higher than last year. This should help prevent a sharp build-up in palm oil stocks during the upcoming peak production season.

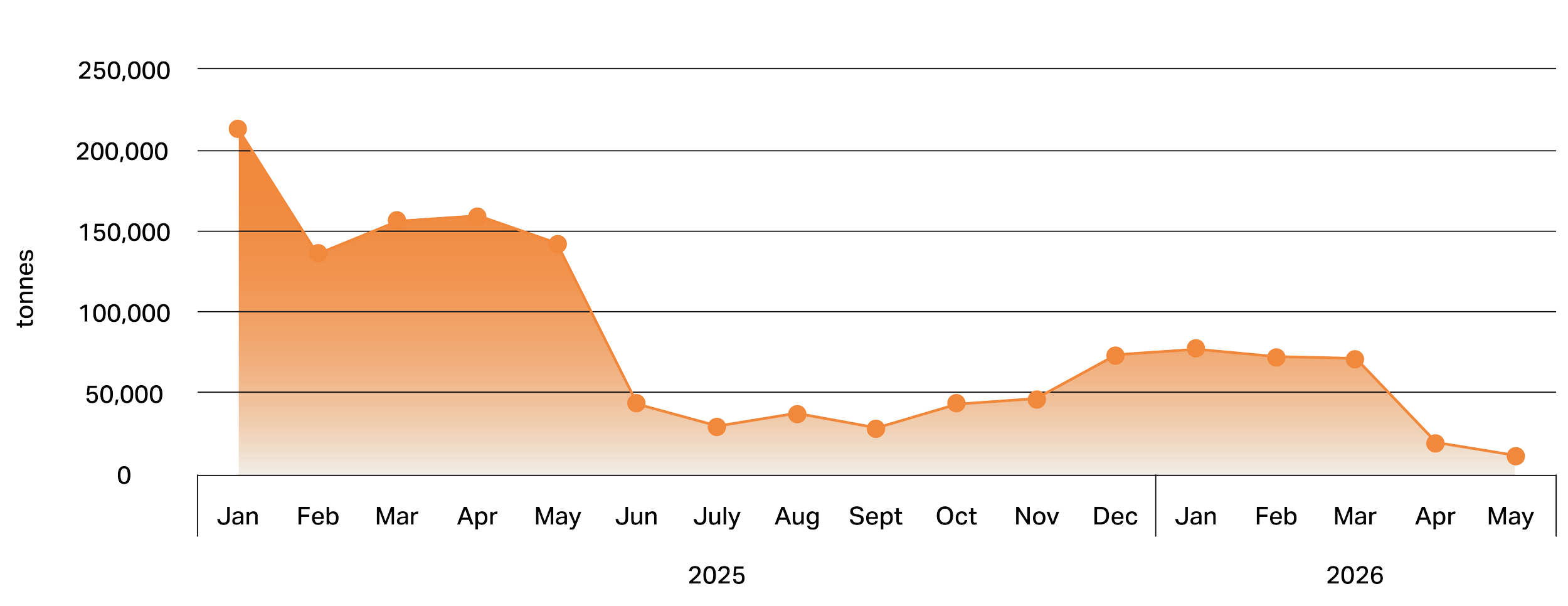

US Soybean Oil Exports

Figure 5: US soybean oil exports (Oil World, 2026).

Palm Oil Price Outlook: Tightening Indonesian Supply and El Nino Risks to Support Prices

In the first half of 2026, US soybean oil and rapeseed oil led the vegetable oil complex, rising by 59% and 16% year-to-date, respectively. The rally was driven by the US biofuel mandate and restrictions under the 45Z biofuel tax credit programme, which favour North American (US and Canadian) feedstocks. By comparison, South American soybean oil, sunflower oil and Malaysian palm oil prices recorded more modest gains of between 8% and 10%.

The unusually high premium of US soybean oil since March 2026 has significantly reduced its export competitiveness. US soybean oil exports fell to just 11,000 tonnes in May 2026, the lowest level in 19 months (see Figure 5). Exports are expected to remain subdued if this premium persists, leaving global importers increasingly dependent on South American supplies.

As of mid-June, US soybean oil was trading at a premium of USD580 per tonne over Argentine soybean oil.

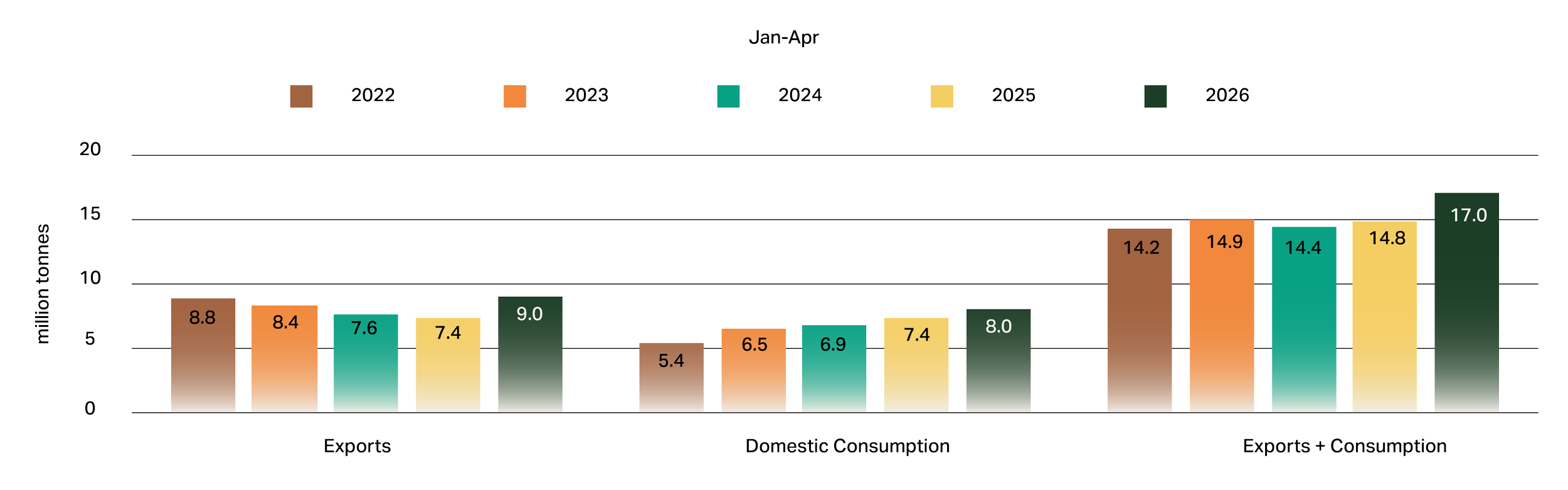

Indonesia’s Palm Oil Exports and Domestic Consumption, from January to April

Figure 6: Indonesia’s palm oil exports and domestic consumption, from January to April (Oil World, Gapki, 2026).

At the same time, Indonesia’s exportable palm oil supply is expected to tighten from late Q3 into Q4, as the B50 biodiesel mandate takes effect in July 2026 against a backdrop of stagnant production and stronger front-loaded demand. Oil World projects Indonesia’s palm oil production to remain broadly unchanged at 49.4 million tonnes in 2026, while exports and domestic consumption during the first four months of the year increased by a combined 15% or 2.2 million tonnes (see Figure 6).

This development may encourage global importers to shift part of their sourcing towards Malaysia in pursuit of greater supply stability.

Elevated fertiliser costs following the US-Iran conflict may also discourage fertiliser application among smallholders in Malaysia and Indonesia. However, the impact of lower fertiliser usage would only become evident after a time lag.

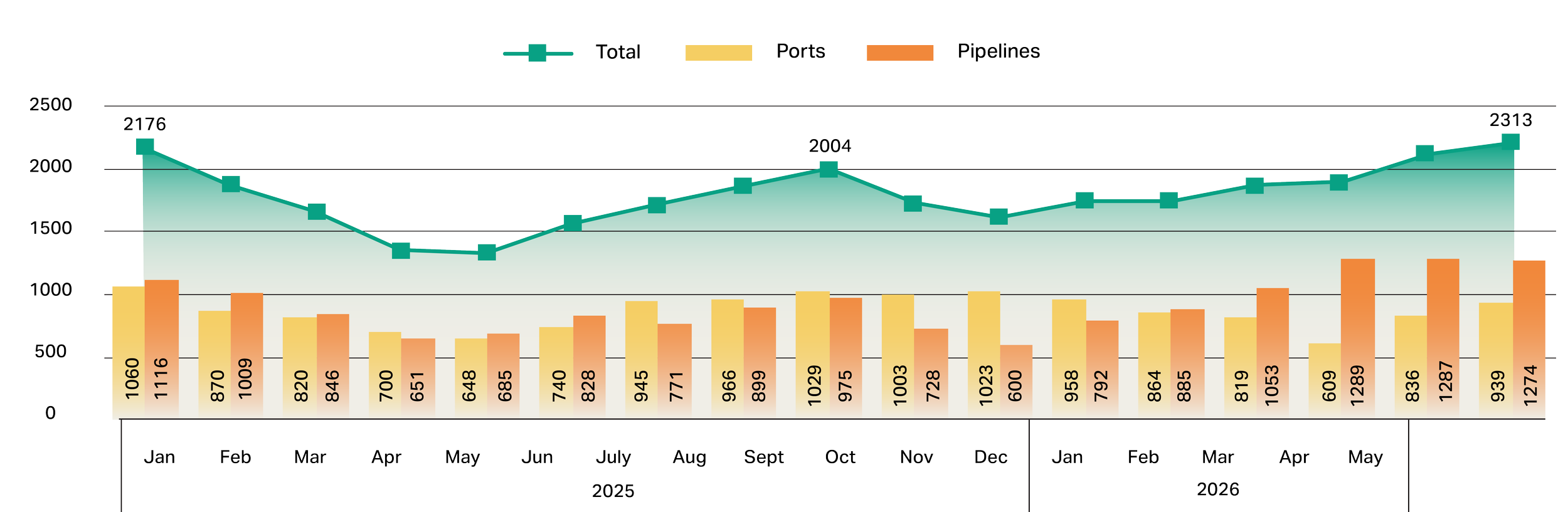

At the same time, vegetable oil stocks in major importing markets have risen sharply, reflecting weaker near-term consumption amid inflationary pressures. India’s vegetable oil stocks reached a 17-month high of 2.2 million tonnes in May (see Figure 7), while China’s vegetable oil inventories climbed to nearly 2.0 million tonnes, the highest level recorded in 2026.

Elevated inventories in both markets could temporarily slow import demand in the near term.

India’s Vegetable Oil Stocks at Ports & Pipelines (in ‘000 tonnes)

Figure 7: India’s vegetable oil stocks (Solvent Extractors’ Association of India, 2026).

Looking ahead, crude palm oil prices are expected to trade between RM4,400 (USD1,062) and RM4,650 (USD1,123) per tonne in July, supported by a tightening supply outlook in Indonesia and increasing El Nino risk. Although oil palm plantations in Malaysia and Indonesia had not yet been affected as of June, the likelihood of a stronger El Nino emerging from July or August is increasing.

A strong El Nino could reduce rainfall and bring drier conditions across Southeast Asia, Australia and India. However, any impact on palm oil yields and production would only become evident after a lag of nine to twelve months.

Nevertheless, further price gains may be capped by elevated vegetable oil inventories in key importing markets. Biodiesel economics have also become less supportive, as gasoil prices have fallen below palm oil prices in the futures market.

Exchange Rate: USD1 = RM4.14