CPO Prices to Stay Firm Around RM4,400 (USD1,106) Amid Tight Exportable Supply and Weather Risks

Crude palm oil (CPO) prices consolidated within a lower range in May amid cautious market sentiment, as the West Asia conflict entered its fourth month. Geopolitical tensions continue to disrupt trade flows, with shipments moving through the Strait of Hormuz remaining constrained. Energy prices therefore remain elevated, with crude oil and gas oil trading around 50% and 40% higher respectively, as of mid-May, compared with levels recorded on 27 February.

Heading into June, palm oil prices are expected to be shaped by the following key factors:

Improved Price Competitiveness

Palm oil remains the most competitively priced vegetable oil in India. Meanwhile, in the US market, soybean oil prices rose in May to their highest level since November 2022, trading sharply above other major vegetable oils and keeping the overall vegetable oil complex supported.Tight Exportable Supply

Reduced exportable palm oil supply between April and September 2026 is expected to keep prices firm. Oil World projects Malaysia’s palm oil exports to rise by 390,000 tonnes in Q2 and Q3, while Indonesia’s exports are forecast to decline by 1.7 million tonnes over the same period.Rising Oilseed Supply

A sharp increase in oilseed production is shaping up for the 2026/27 season. Combined soybean, sunflower seed and rapeseed production is projected to rise by 22.4 million tonnes to a record 600 million tonnes.

A Brief Market Recap

The Malaysian government announced the implementation of B15 biodiesel beginning 1 June. Around 70% of fuel depots nationwide are able to carry out blending using existing infrastructure, while the remaining 30% will require operational adjustments ahead of the transition.

The UAE has officially exited OPEC and OPEC+ effective 1 May, seeking greater flexibility to accelerate crude oil production once the West Asia conflict eases. Under OPEC, the UAE had been allocated a quota of 3.0-3.5 million barrels per day, well below its production capacity of 4.8 million barrels per day. The near-term impact is expected to remain limited given ongoing disruptions at the Strait of Hormuz, though analysts believe the move could weigh on oil prices once geopolitical tensions subside.

The European Commission also adopted a delegated regulation updating the methodology and data for high indirect land use change (ILUC) risk biofuels. According to a USDA report, the revised methodology would effectively phase out soybean as a biofuel feedstock by 2030. The regulation will now proceed to the European Parliament and Council for further consideration.

Malaysia's Palm Oil Supply and Demand for April 2026

Table 1: Monthly statistics of Malaysian palm oil for April 2026 (MPOB, 2026).

Palm Oil Supply and Demand Dynamics in June: Key Changes and Trends

Malaysia’s palm oil stocks recovered marginally to 2.31 million tonnes in April, supported by a seasonal increase in production. Palm oil production typically trends higher between March and October, as drier weather conditions improve harvesting productivity and fresh fruit bunches yield higher oil extraction rates.

Cumulative exports from January to April 2026 rose by 25.5% (+1.1 million tonnes) to 5.38 million tonnes, marking the highest level since 2019. However, exports declined by 14.3% month-on-month in April to 1.30 million tonnes. Despite the monthly decline, exports remained firm, accounting for 80% of Malaysia’s palm oil production during the month.

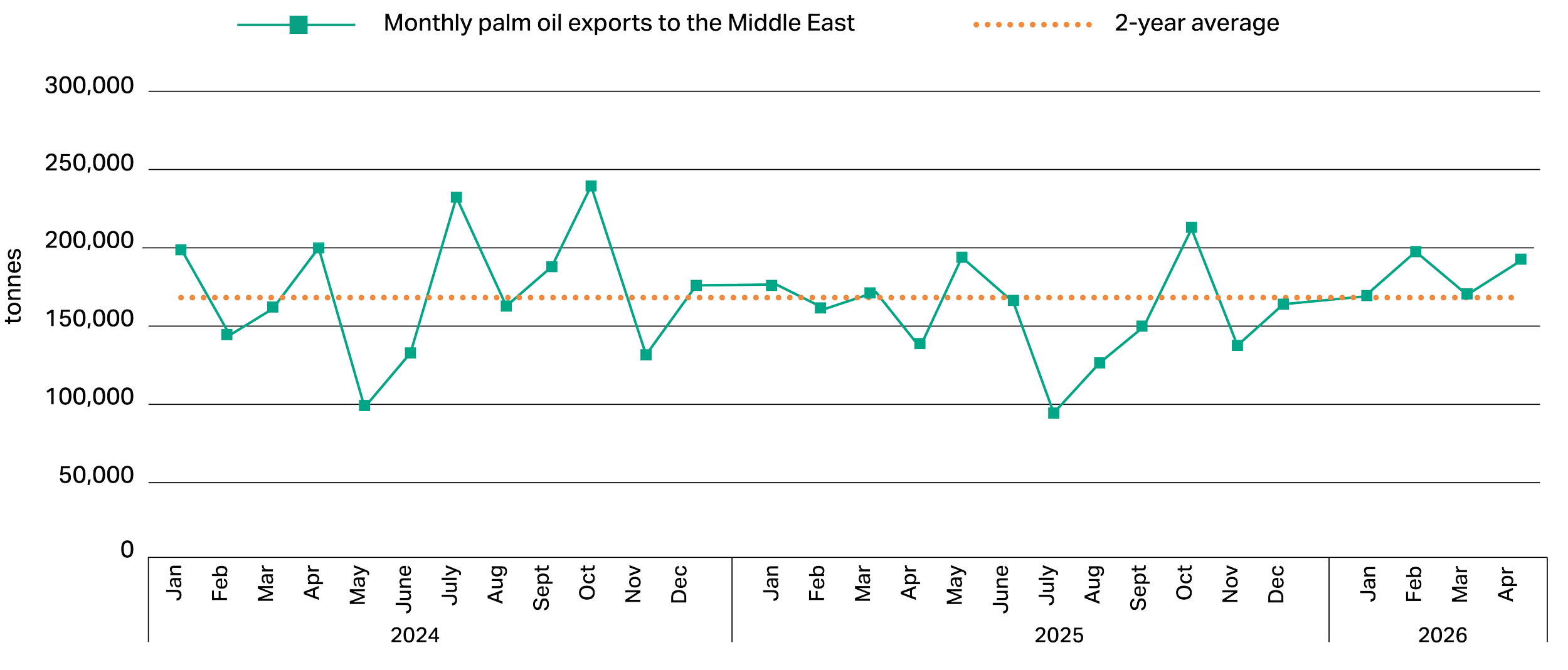

Malaysian Palm Oil Exports to the Middle East

Figure 3: Malaysian palm oil exports to the Middle East, from 2024 to 2026 (MPOB, 2026).

Malaysian palm oil exports to the Middle East also remained above average in March and April (see Figure 3), despite disruptions at the Strait of Hormuz. Cargoes that would traditionally discharge at Gulf ports within Hormuz are increasingly being rerouted via alternative ports including Jeddah and Aqaba along the Red Sea, as well as Sohar and Khor Fakkan outside Hormuz.

In the coming months, Malaysian palm oil exports may temporarily soften in May and June but are expected to strengthen again between July and September as Indonesia’s B50 biodiesel mandate takes effect. As a result, a sharp build-up in palm oil stocks is considered unlikely during the upcoming peak production season in Southeast Asia.

Palm Oil Price Outlook: Weather Risks and Biofuel Demand Keep Prices Firm

Soybean oil prices in the US market rose to their highest level since November 2022 in mid-May, making it the most expensive major vegetable oil globally. During this period, US soybean oil traded at a premium of USD523 per tonne over Southeast Asian palm oil, US393 per tonne above Black Sea sunflower oil and USD303 per tonne over EU rapeseed oil.

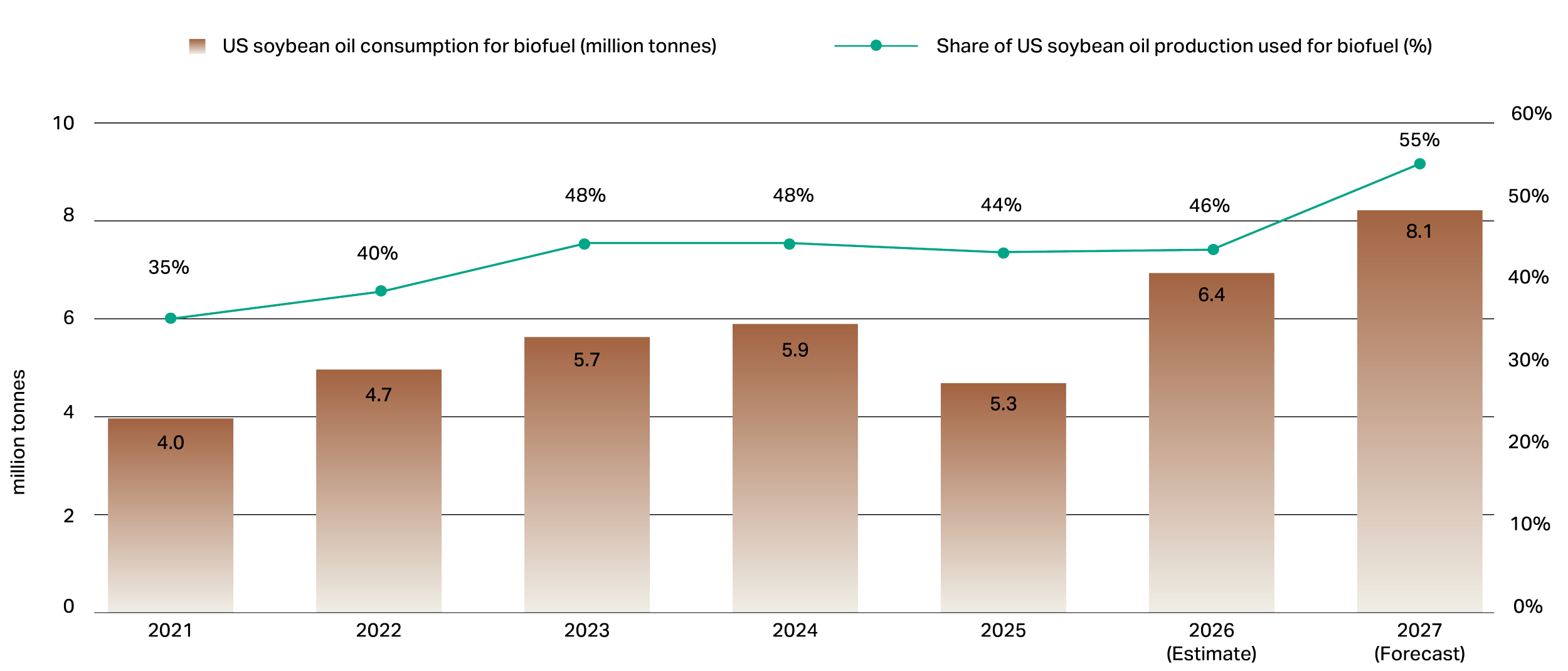

US Soybean Oil Consumption for Biofuel

Figure 4: US soybean oil consumption for biofuel, from 2021 to 2027F (USDA, 2026).

Strong soybean oil demand from the US biofuel sector has continued to support prices. The USDA projects US soybean oil consumption at 13.5 million tonnes in 2026 and 14.8 million tonnes in 2027. Figure 4 shows that soybean oil usage in the US biofuel sector is expected to rise further to 55% of total production, compared with 44% in 2025—representing a sharp increase of 2.8 million tonnes.

Recent developments in the US biofuel market have improved palm oil’s price competitiveness across major importing markets. Palm oil remains the most competitively priced vegetable oil in India, while Malaysian palm olein was also trading at a marginal discount to Argentine soybean oil—a pricing dynamic that should continue supporting palm oil demand.

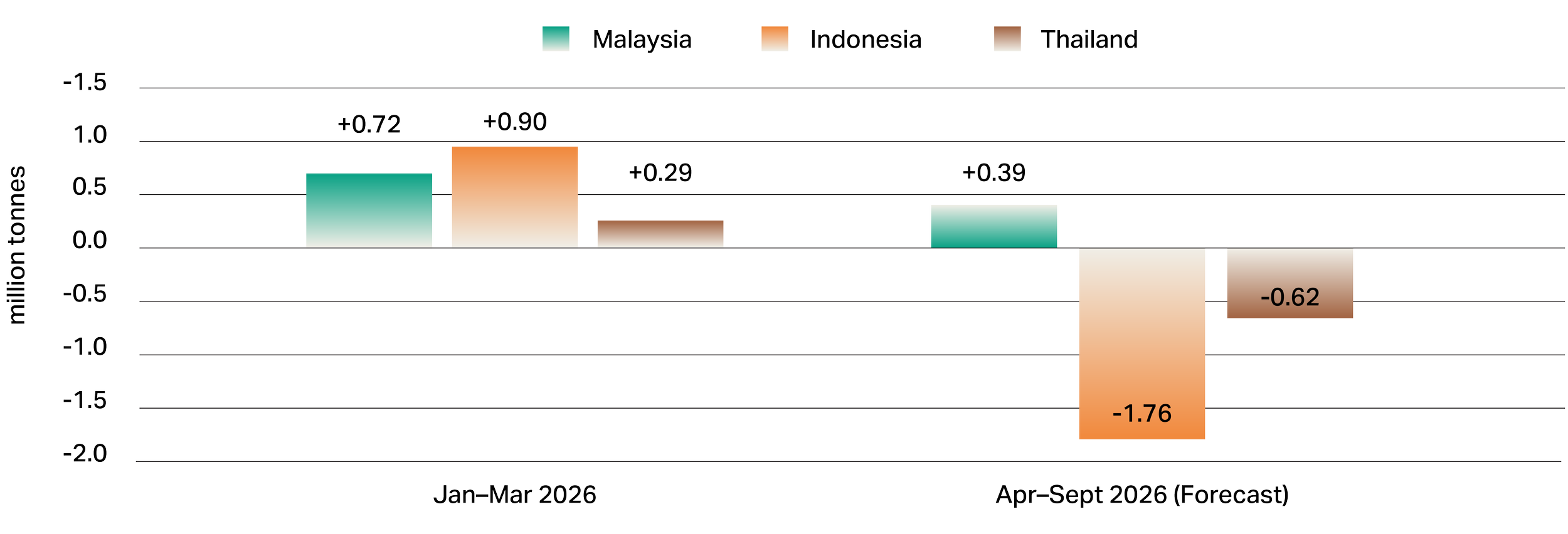

Year-on-Year Change in Palm Oil Exports, 2025 versus 2026

Figure 5: Southeast Asia palm oil export changes, 2025 versus 2026 (Oil World, 2026).

In Q1 2026, combined palm oil exports from Malaysia, Indonesia and Thailand rose by 1.9 million tonnes. However, this trend is expected to reverse between April and September, with Oil World projecting combined exports from the three countries to decline by 2 million tonnes in Q2 and Q3, primarily due to lower Indonesian exports.

Malaysia’s exports are projected to rise by 390,000 tonnes during the period, while Indonesia’s exports are forecast to decline by 1.7 million tonnes as more palm oil is redirected towards domestic energy usage (see Figure 5). Thailand’s palm oil exports are also expected to decline by 620,000 tonnes after the country tightened export controls for one year beginning in April to ensure sufficient domestic supply.

The USDA has also released its first estimates for global oilseed production in the 2026/27 season, with all three major oilseeds projected to reach record highs. Global soybean production is forecast to rise by 14 million tonnes, sunflower seed by 7 million tonnes and rapeseed by 1.4 million tonnes. Collectively, production of these three oilseeds is expected to increase by 4%, or 22.4 million tonnes, to a record 600 million tonnes.

Looking ahead, crude palm oil prices are expected to remain supported around RM4,400 (USD1,106) per tonne in June, as global biofuel policies continue to provide the main source of market support. Vegetable oil prices still retain bullish potential, as the recent price correction was likely driven by profit-taking activity among funds and speculators.

Supply risks also remain elevated due to unresolved geopolitical tensions and the increasing likelihood of El Nino conditions, both of which could add further uncertainty to global vegetable oil supply in the upcoming season. El Nino typically brings drier-than-normal weather conditions to Southeast Asia, reducing rainfall and soil moisture levels, which may affect regional agricultural production. The Malaysian Meteorological Department expects El Nino conditions to develop between June and July, potentially persisting into early 2027.

Exchange Rate: USD1 = RM3.98