Analysis on March 2026: CPO to Consolidate at RM4,000–RM4,300, on Firm Soybean Oil Prices

Crude palm oil (CPO) prices remained broadly stable in February, trading within a range of RM3,990 to RM4,225 (USD1,025–USD1,086), and this range-bound movement is expected to persist into March. Downside risks to palm oil prices appear limited in the near-term, as January trade flows suggest that vegetable oil demand has shifted towards palm oil due to favourable price differentials, alongside positive sentiment in the soybean oil market.

Heading into March, palm oil prices are expected to be shaped by the following key factors:

Production Growth to Moderate from Q2

Malaysia’s strong year-on-year production growth in January 2026 is likely to be temporary, with output expected to ease from Q2 onwards. This anticipated slowdown, together with improving Malaysian exports and Indonesia’s front-loading of shipments ahead of the March export levy increase, is expected to reduce palm oil stocks in both countries.US Soybean Oil Strength Supports Palm Oil

Strength in US soybean oil prices is expected to continue supporting palm oil. Soybean oil prices in the US rallied by 17% in February, driven by optimism surrounding US biofuel policy scheduled for announcement in March 2026.Rising China Soybean Oil Exports May Cap Upside

Gains in palm oil prices may be partially capped by rising soybean crushing, particularly in China. The country became a net exporter of soybean oil for the first time in 2025 and is expected to maintain this position in 2026.

A Brief Market Recap

Indonesia has imposed restrictions on the export of palm oil waste, including used cooking oil (UCO), palm oil mill effluent (POME) and high-acid palm oil residue (HAPOR) in order to secure feedstock for its domestic biodiesel programme. The regulation took effect in February 2026, with only exporters holding prior approval permitted to continue shipments until their existing permits expire.

China has resumed purchases of Canadian canola seed under a new trade agreement that reduces import tariffs from 84% to 15%, effective March 2026. In return, Canada will grant a quota of 49,000 Chinese electrical vehicle (EVs) at a most-favoured-nation (MFN) import tariff of 6.1%.

US President Donald Trump has announced a new global tariff following a US Supreme Court ruling that struck down many of the reciprocal tariffs imposed last year. The new measure may remain in force for up to 150 days while the administration conducts a trade investigation aimed at challenging the Court’s decision.

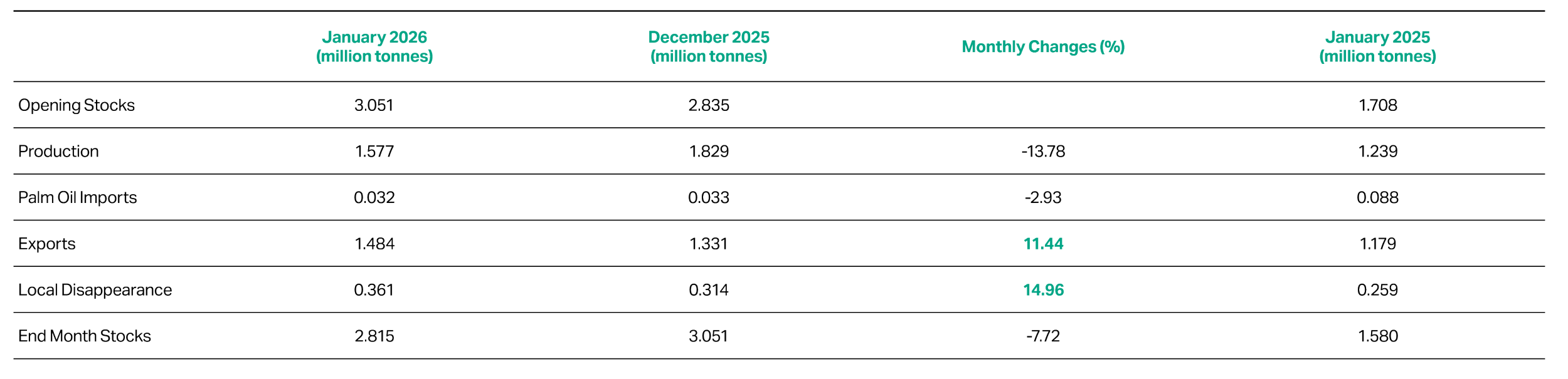

Malaysia's Palm Oil Supply and Demand for January 2026

Table 3: Monthly statistics of Malaysian palm oil for January 2026 (MPOB, 2026).

Palm Oil Supply and Demand Dynamics in March: Key Changes and Trends

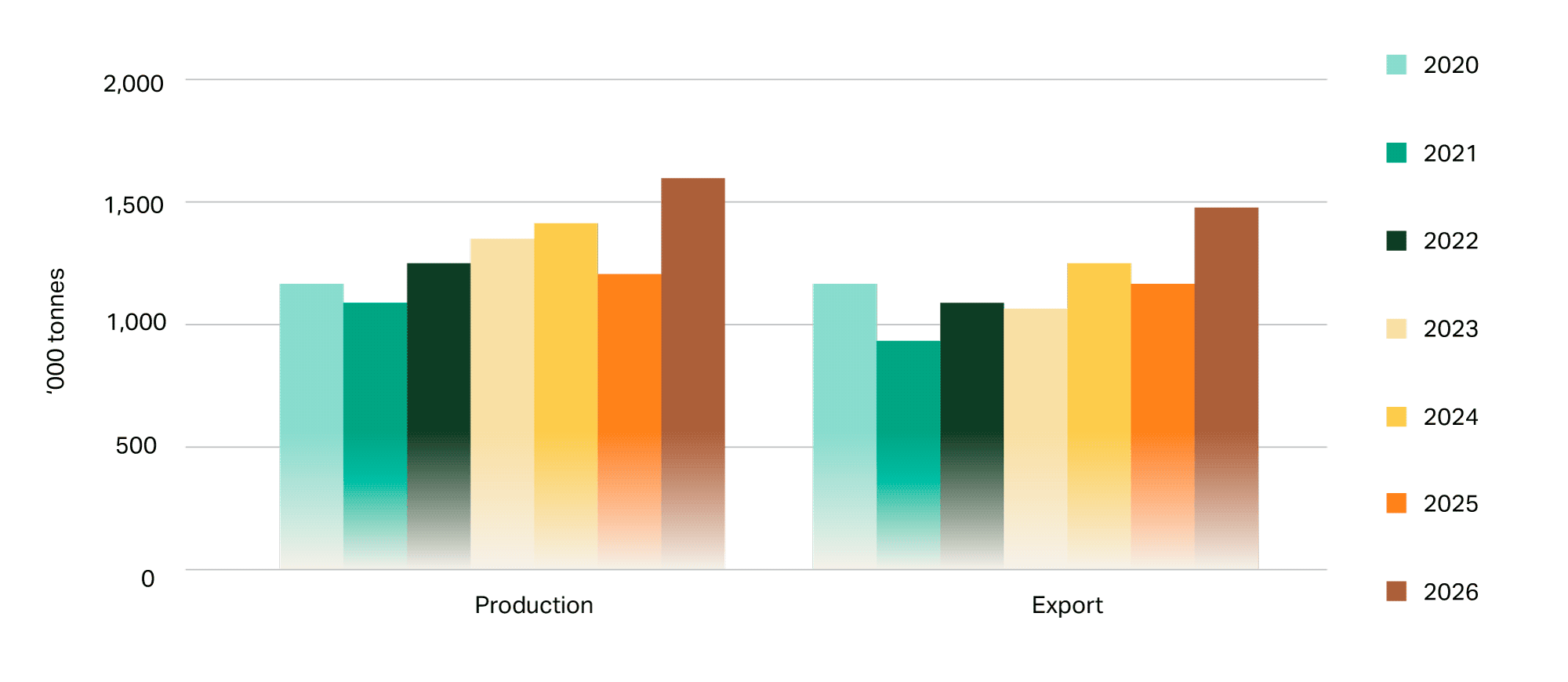

Malaysia’s palm oil production eased seasonally to 1.58 million tonnes in January, down 13.8% (252,000 tonnes) month-on-month but up 27.3% (338,000 tonnes) compared with January 2025. The strong production momentum observed in Q4 2025 carried into early 2026, with Sabah recording the largest increase at 33.5%, followed by Peninsular Malaysia at 29.3% and Sarawak at 16.8%.

Historically, January production has averaged about 1.33 million tonnes over the past decade, with only 2018 and 2019 exceeding the 1.5 million-tonne level.

Meanwhile, exports strengthened to 1.48 million tonnes, up 11.4% (153,000 tonnes) from December, marking the second-highest monthly export volume in the past 12 months. The increase was driven primarily by stronger demand from India and Egypt, with shipments to India reaching a 15-month high and exports to Egypt climbing to a 13-month high.

Malaysian Palm Oil Production and Exports for January from 2020 to 2026

Figure 2: Malaysian palm oil production and exports for January from 2020 to 2026 (MPOB, 2026).

As a result, palm oil stocks declined 7.7% to 2.81 million tonnes. Both production and exports in Malaysia reached their highest January levels since 2020 (see Figure 2), underscoring improving supply and demand dynamics. In January 2026, Malaysia’s palm oil exports accounted for 94% of production, compared with 72% in December 2025.

Looking ahead, exports in Q1 2026 are expected to outperform the same period last year, supported by a shift in relative price dynamics. In Q1 2025, palm oil traded at a USD112 premium over soybean oil in the global market. This trend reversed in the first two months of 2026, with palm oil trading at a discount to soybean oil. Improved price competitiveness has encouraged stronger import demand from key consuming markets.

Palm Oil Price Outlook: Demand Recovery and Soybean Oil Strength to Provide Support

Vegetable oil prices remained well supported in February, underpinned by optimism surrounding US biofuel policy and firmer crude oil prices amid escalating geopolitical tensions between the US and Iran. Brent crude oil prices rebounded by 17% year-to-date to USD72 in February, while prices of the four major vegetable oils increased by between 1% and 7% over the same period.

Palm oil fundamentals are expected to improve gradually in the coming months. Firmer Malaysian exports in Q1 and Indonesia’s front-loading of shipments in January and February ahead of the March export levy increase are projected to reduce palm oil inventories in both countries.

On the demand side, India is expected to shift its consumption back towards palm oil following improved price competitiveness since late 2025. Palm oil consumption in India is forecast to rise by 800,000 tonnes in 2026, while soybean and sunflower oil consumption is expected to decline by a combined 400,000 tonnes. January 2026 data already reflect this shift, with India’s palm oil imports rising to a four-month high while soybean oil imports fell to an 11-month low. This trend is likely to persist through the remainder of Q1 2026.

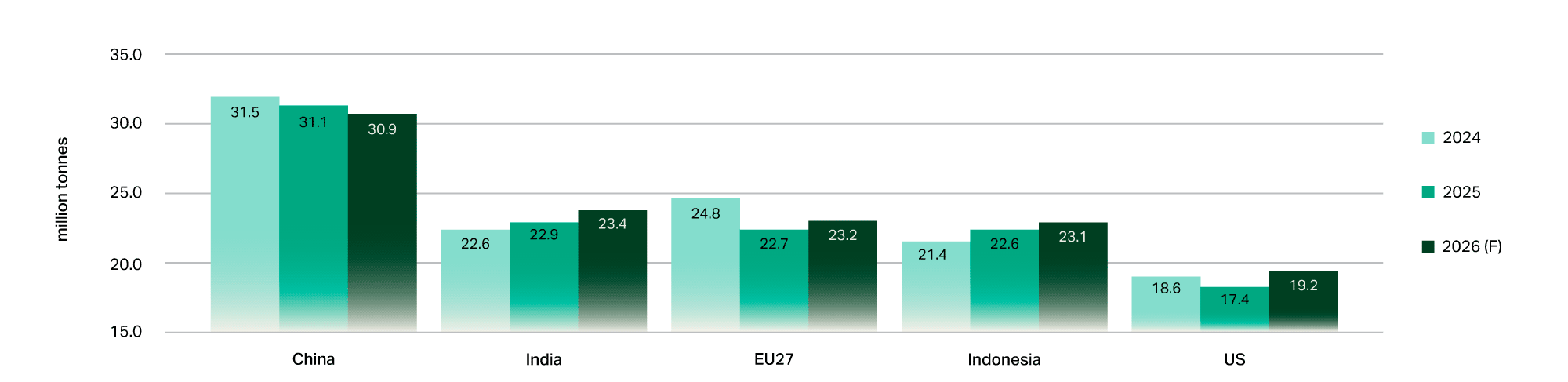

Consumption of Palm, Soybean, Sunflower & Rapeseed Oils in Major Markets (million tonnes)

Figure 3: Consumption of the four major vegetable oils in major markets (Oil World, 2026).

Among the five major vegetable oil consuming markets—China, India, EU27, Indonesia and the US—the US is expected to lead growth in 2026. Total consumption of palm, soybean, rapeseed and sunflower oil in the US is projected to rise by 1.8 million tonnes (see Figure 3). Meanwhile, India, EU27 and Indonesia are each projected to record increases of around 500,000 tonnes. Rising consumption across these markets is expected to continue supporting vegetable oil prices in the months ahead.

Optimism over US biofuel policy, which favours domestically produced soybean oil, has further lifted prices. US soybean oil rallied by 17% in February, trading at a significant premium of USD172 over Argentine-origin soybean oil. The sustained strength in US soybean oil prices is likely to continue providing support to palm oil prices.

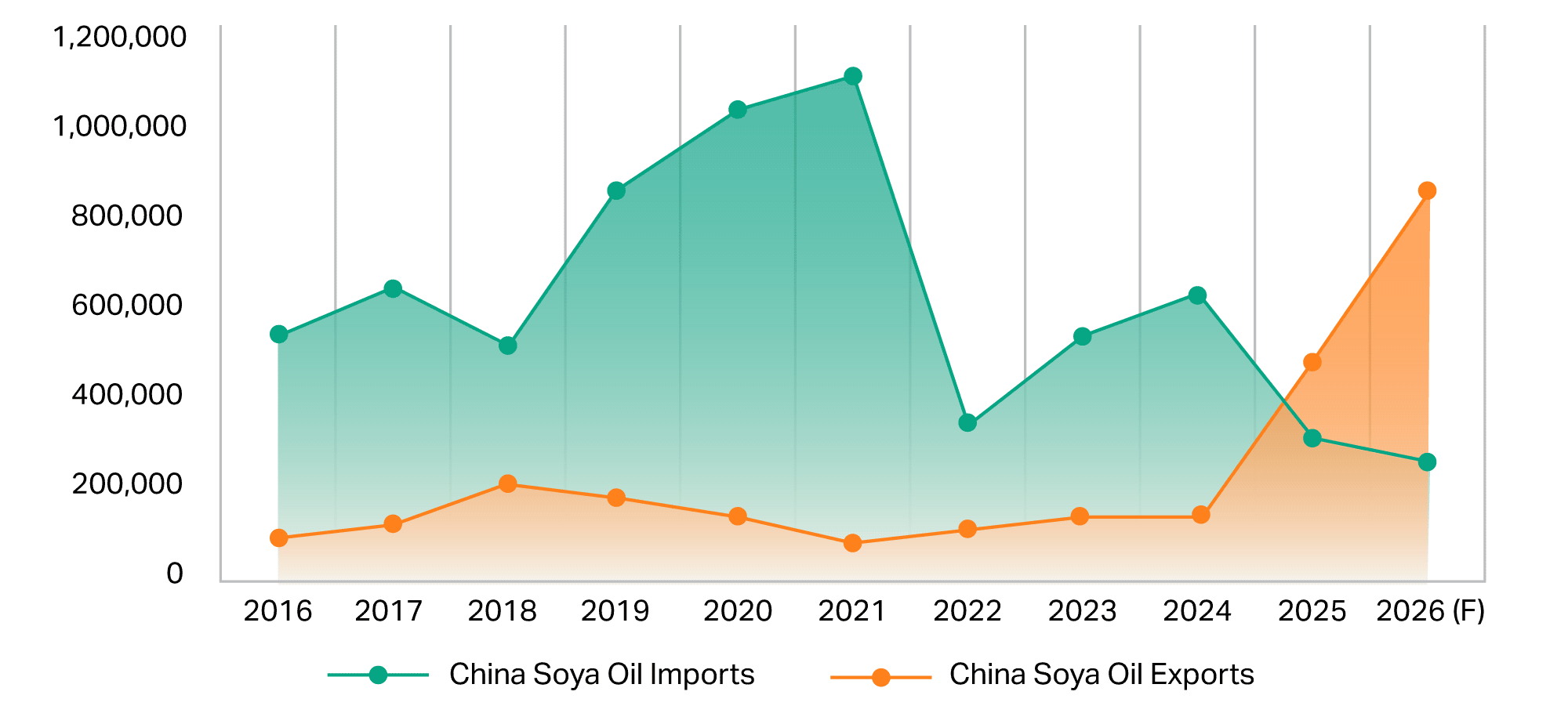

China Soybean Oil Imports and Exports from 2016 to 2026

Figure 4: China soybean oil imports and exports from 2016 to 2026 (F) (Oil World, 2026).

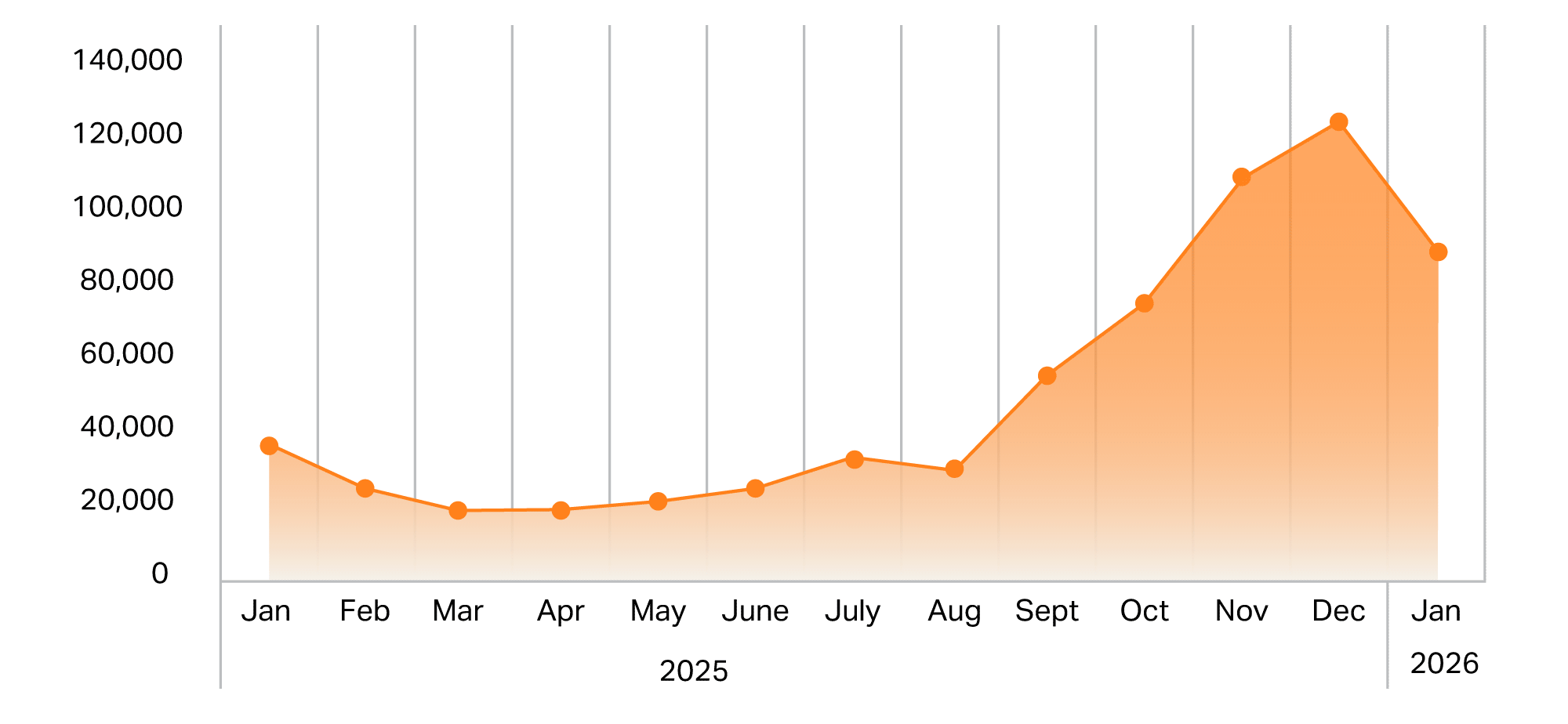

China Monthly Soybean Oil Exports

Figure 5: China monthly soybean oil exports (China Customs, 2026).

Despite these supportive factors, upside potential in palm oil prices may be partially capped by rising soybean crushing, particularly in China. The country became a net exporter of soybean oil for the first time in 2025 and is expected to maintain this position in 2026, with exports projected at around 850,000 tonnes (see Figure 4). Monthly soybean oil exports exceeded 100,000 tonnes in both November and December 2025, reflecting slower domestic demand. India accounted for nearly half of China’s soybean oil exports last year.

Tightening near-term supply, improving Indian demand and firm US soybean oil prices should keep palm oil prices supported. However, ample global soybean supply and rising Chinese soybean oil exports may limit gains. Palm oil prices are therefore projected to consolidate within the range of RM4,000–RM4,300 (USD1,028–USD1,105) per tonne in March.

Exchange Rate: USD1 = RM3.89