Inside China’s Expanding Specialty Fats Market: Opportunities for Palm-Based Ingredients

China’s specialty fats market is now valued at USD16.4 billion (RMB114.85 billion) and is projected to reach USD22.8 billion (RMB159.59 billion) by 2030. For palm-based suppliers, the question is no longer whether the opportunity exists, but which segments are growing the fastest.Part 1

China is one of the world’s largest producers and consumers of oils and fats. Within this vast market lies a high-value segment that has quietly emerged as one of the most attractive destinations for palm-based products: specialty fats. These specialty fats—including cocoa butter alternatives, shortenings, margarines, non-dairy creamers, milk fat substitutes and powdered fats—provide the functionality that gives a chocolate its snap, croissants their flaky layers, and milk-tea cream-toppings their stability. Occupying the higher-value end of the oils and fats value chain, specialty fats are experiencing robust and sustained growth.

According to a recent market study on China’s palm-based specialty fats industry commissioned by MPOC, the market was valued at an estimated USD16.4 billion (RMB114.85 billion) in 2025, representing year-on-year growth of 6.14%. The outlook remains highly positive, with the market forecast to expand from USD17.5 billion (RMB122.66 billion) in 2026 to USD22.8 billion (RMB159.59 billion) by 2030, reflecting a compound annual growth rate (CAGR) of 6.8%. For Malaysian exporters assessing growth opportunities, this article explores the size, structure and dynamics of the market. The upcoming second instalment will examine competition and strategic considerations.

China's Specialty Oils & Fats Market, 2024–2030F

Figure 1: China’s total specialty fats market, from 2024 to 2030, in USD billion (HMC Consulting, 2025).

Three Forces Driving Market Growth

The study identifies three key factors underpinning the market’s momentum.

The first is consumption upgrading and growing health-consciousness among consumers, which are increasing demand for premium and functional fats. The second is the continued expansion of China’s food manufacturing and advanced downstream sectors, which rely heavily on high-quality oils and fats as key inputs. The third is the combined effect of supportive policies and technological advancement, as domestic manufacturers achieve breakthroughs in modification technologies and greener production processes.

Underpinning these developments is China’s structural dependence on imported raw material. As palm oil is not domestically produced in China, the country relies entirely on imports for its palm oil requirements. China’s overall edible oil self-sufficiency rate remains around 38.5%, creating a significant supply gap and a strategic opportunity for palm oil-producing countries.

Palm and Palm Kernel Oil: Core Ingredients in Specialty Oils and Fats

The specialty fats market expanded by 6.14% in 2025, reaching USD16.4 billion (RMB114.85 billion), up from USD15.5 billion (RMB108.2 billion) in 2024. Within this market, palm kernel oil and its derivatives accounted for the largest share, representing 32.4% of total market value, underscoring the central role of palm-based ingredients in the sector.

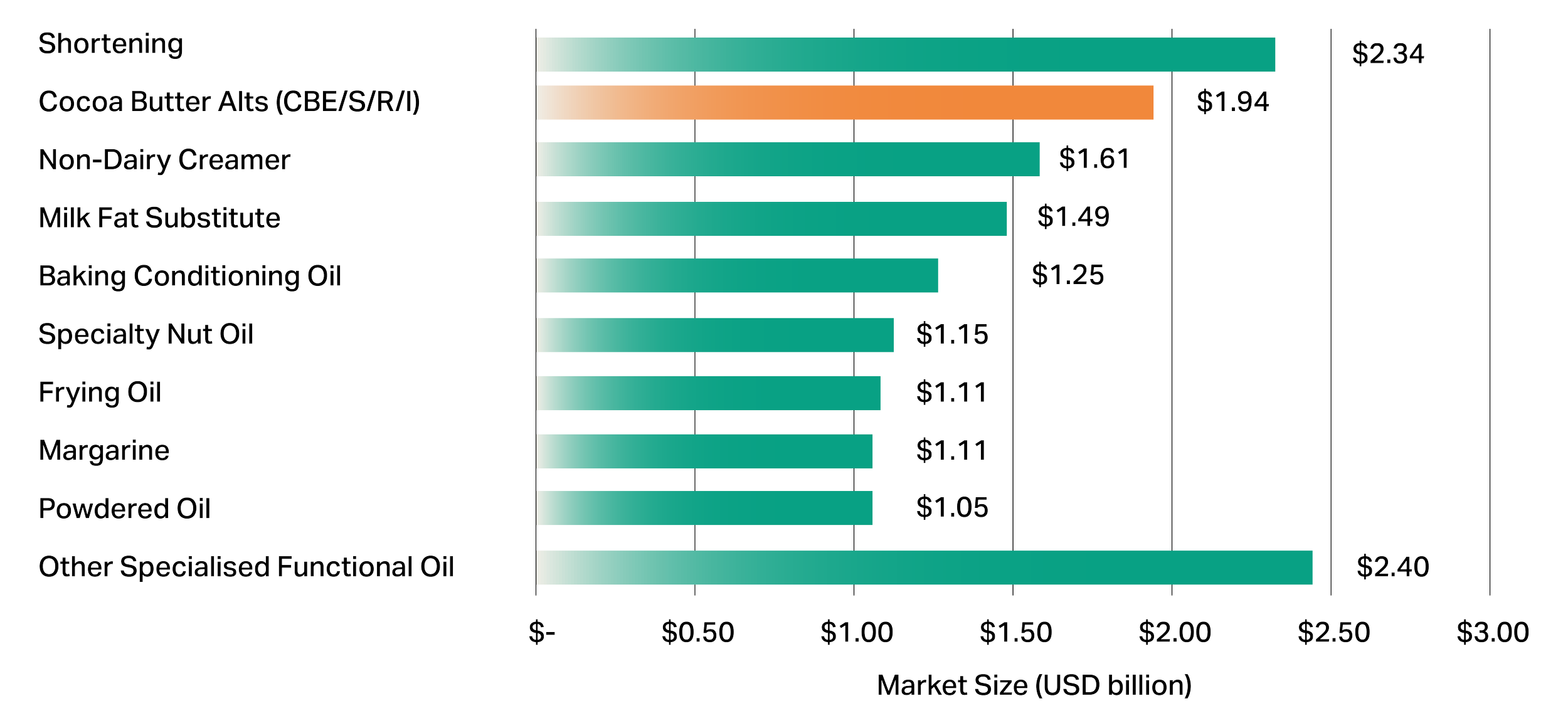

A closer examination of individual product categories further reinforces this importance. Based on the latest available data through 2024, shortening remained the largest segment, valued at USD2.34 billion (RMB16.38 billion), followed by the cocoa butter alternatives category—including cocoa butter equivalents (CBE), cocoa butter substitutes (CBS), cocoa butter replacers (CBR) and cocoa butter improvers (CBI)—with a combined value of USD1.94 billion (RMB13.57 billion). Meanwhile, milk fat substitutes, one of the fastest-growing segments, reached USD1.49 billion (RMB10.43 billion) after recording annual growth of 13.9%.

China Specialty Oils & Fats Market by Category, 2024

Figure 2: China’s food-specific fats market by category in 2024, in USD billion (HMC Consulting, 2025).

Several of these categories align closely with palm oil’s strengths. Cocoa butter equivalents are commonly formulated using palm mid fractions, while cocoa butter substitutes rely heavily on palm kernel oil and coconut oil. Likewise, shortening and margarine often utilise palm oil as a primary feedstock due to its functionality, versatility and cost competitiveness.

Looking ahead, the combined market value of cocoa butter alternatives was estimated at USD2.09 billion (RMB14.63 billion) in 2025, representing growth of 7.8% from 2024. This further reinforces the continued relevance of palm oil and palm kernel oil as foundational ingredients within China’s specialty oils and fats industry.

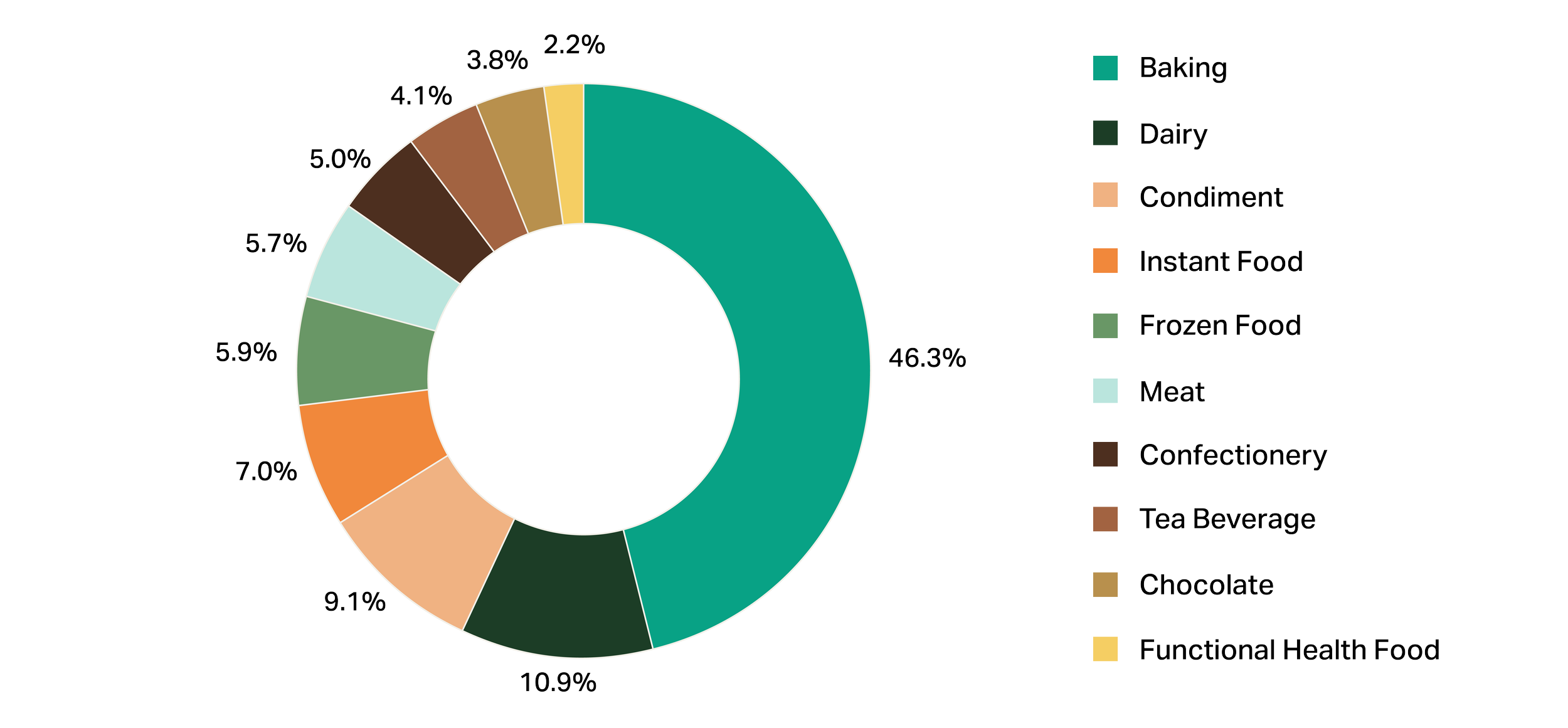

Where Specialty Fats Are Used

Demand for specialty fats is concentrated across a relatively small number of high-volume application sectors. The bakery industry is by far the largest consumer, accounting for 46.3% of total specialty fats demand and representing a market value of USD7.16 billion (RMB50.12 billion) in 2024 alone. Other important sectors include dairy, condiments, instant foods and frozen foods.

The study aptly describes the market dynamic by noting that while the bakery sector defines the scale of demand, the tea beverage sector drives the growth rate. Collectively, four sectors—bakery, confectionery, chocolate and tea beverages—account for 59.2% of total specialty fats consumption.

Where Specialty Fats & Oils Are Used, 2024

Figure 3: China’s food-specific fats market by category in 2024, in USD billion (HMC Consulting, 2025).

The Four Engines of Demand

Each of the four major application sectors presents a distinct growth story and a unique opportunity for palm-based suppliers.

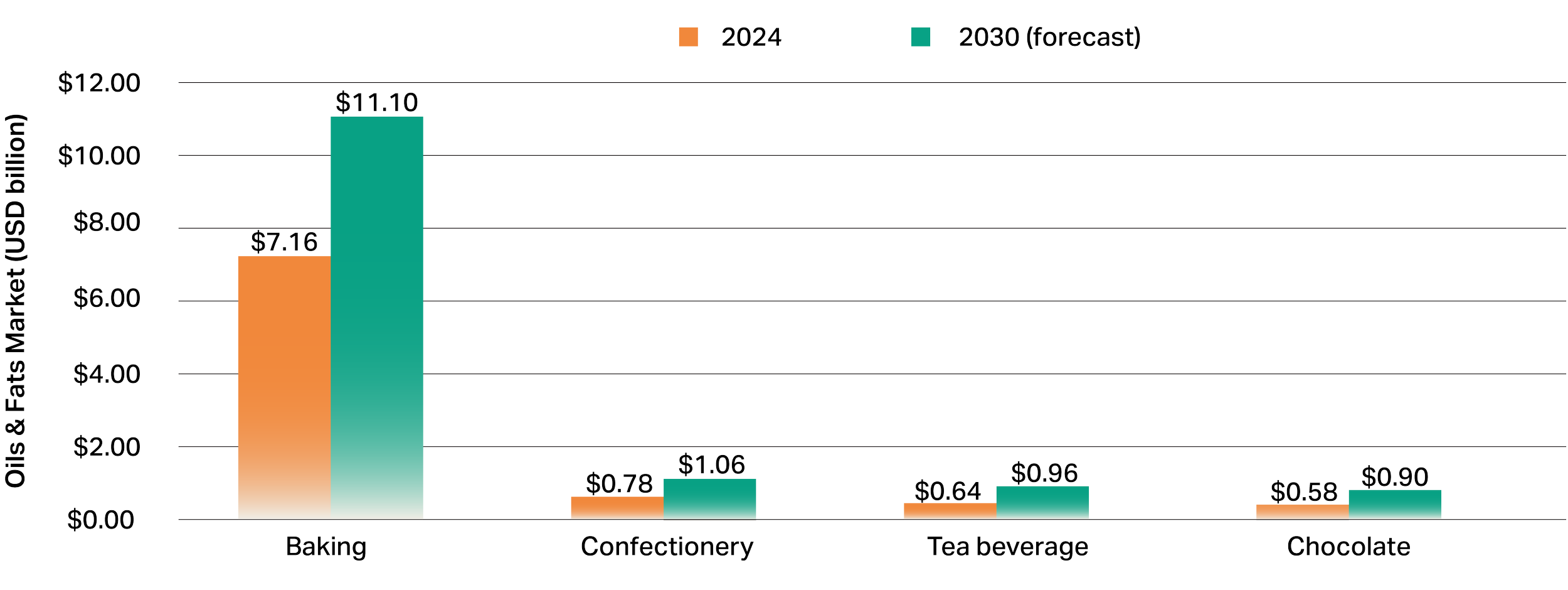

Baking—The Market Anchor

China is the world’s second-largest bakery market, expanding from USD41.1 billion (RMB287.4 billion) in 2020 to USD56.9 billion (RMB398 billion) in 2024. Supported by this strong market growth, demand for bakery fats reached an estimated 1.68 million tonnes in 2024 and is projected to rise to 1.8 million tonnes by 2030, with market value expected to reach USD11.1 billion (RMB77.71 billion).

Palm-based ingredients account for more than 40% of the bakery fats market. Importantly, sales of healthier baking fats increased by 25% in 2024, while zero-trans-fat shortenings are now utilised by approximately 75% of chain bakery brands across China.

Tea Beverages—The Growth Accelerator

The fats segment serving China’s new-style tea beverage industry recorded the fastest growth among all application sectors, expanding at a CAGR of 18.9% between 2020 and 2024 to reach USD640 million (RMB4.48 billion).

With more than 515,000 tea beverage outlets nationwide, cream toppings and cheese foam applications have become significant drivers of specialty fats demand. The sector is forecast to reach USD964 million (RMB6.75 billion) by 2030, growing at a CAGR of approximately 7%.

Confectionery—Upgrading Through Premiumisation

Demand for confectionery fats increased to USD780 million (RMB5.46 billion) in 2024 and is projected to reach USD1.06 billion (RMB7.39 billion) by 2030, equivalent to an estimated demand volume of 650,000 tonnes.

Health and nutrition considerations are increasingly reshaping the category, accelerating the transition away from traditional cocoa butter substitutes towards higher-value cocoa butter equivalents and other premium specialty fats.

Chocolate—A Long-Term Growth Opportunity

Among confectionery-related segments, chocolate fats recorded the strongest historical growth, expanding at a CAGR of 10.9% to reach USD580 million (RMB4.06 billion).

The long-term opportunity lies in China’s relatively low chocolate consumption. Per capita chocolate consumption stands at only 0.25 kg, significantly below the global average of 1.1 kg. As consumption gradually converges towards international levels, demand for premium chocolate products—and consequently high-quality cocoa butter equivalents derived from palm oil—is expected to increase. The chocolate fats market is projected to reach USD896 million (RMB6.27 billion) by 2030, growing at a CAGR of 7.5%.

Specialty Fats Demand by Application, 2024 versus 2030

Figure 4: Specialty fats demand by application, 2024 versus 2030 forecast, in USD billion (HMC Consulting, 2025).

A Market Shaped by Health, Functionality and Premiumisation

Across virtually every segment, demand is increasingly being driven by three interconnected themes: health, functionality and premiumisation. Zero-trans-fat, plant-based and nutrient-fortified products are among the fastest-growing categories, with sales of healthier specialty fats rising by 25% in 2024 alone. Between 2026 and 2040, demand for healthy and functional fats is expected to grow by 12-15% annually—approximately double the pace of the overall market.

For palm-based suppliers, this is perhaps the most important takeaway. China’s specialty fats market is not only expanding in size but also evolving in composition. Many of its fastest-growing segments—including zero-trans-fat bakery fats, plant-based tea beverage creams and premium CBE for chocolate applications—align closely with areas where palm-based ingredients offer strong advantages in functionality, performance and value.

The opportunity is substantial. The next challenge is how Malaysian suppliers can secure and expand their market share amid intensifying competition from both domestic and regional players— a subject that will be explored in Part 2.